When Politics, Violations, and Debt Collide: NYC Rent-Stabilization dilemma

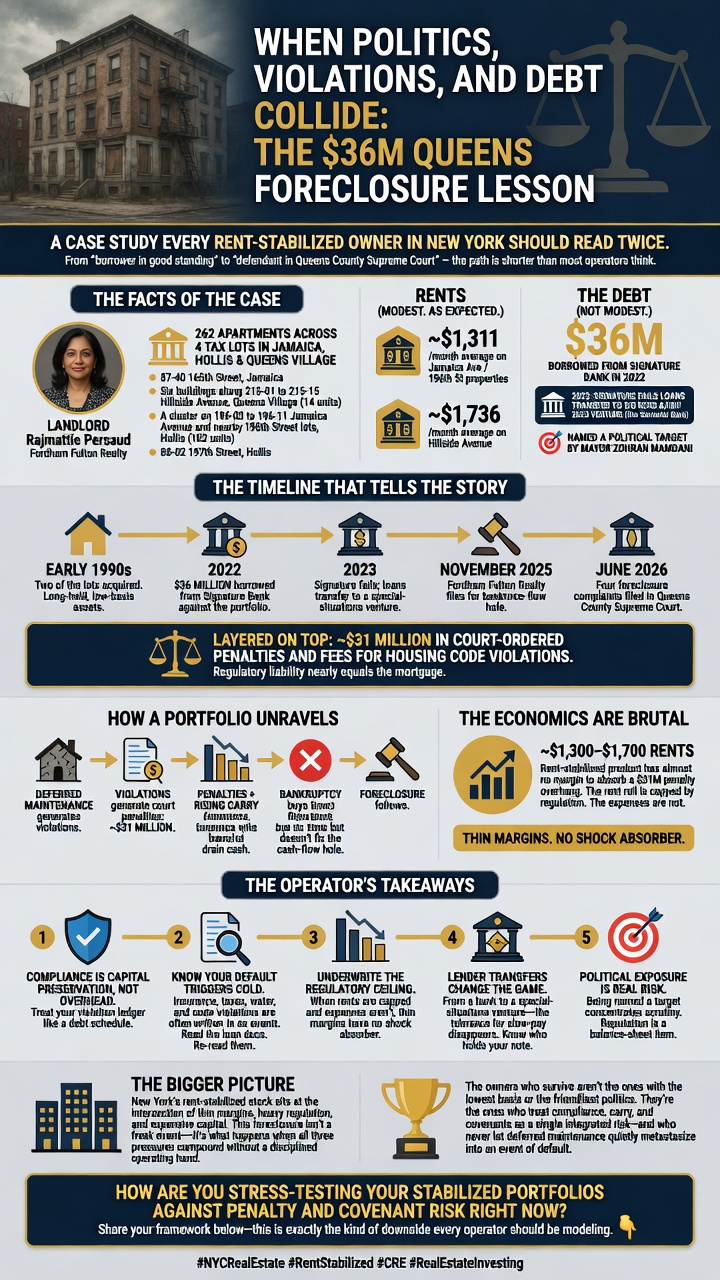

Here’s a story every rent-stabilized owner in New York should read twice. A Queens landlord who became a political target is now staring down four foreclosure cases on roughly $36 million in loans — and the path from “borrower in good standing” to “defendant in Queens County Supreme Court” is shorter, and more instructive, than most operators want to admit.

This isn’t schadenfreude. It’s a case study. In the next few minutes you’ll see exactly how deferred maintenance, regulatory penalties, and debt service can compound into a foreclosure spiral — and what disciplined owners should take from it. The mechanics here are universal, even if the headline is specific.

🔍 The Facts of the Case

The landlord is Rajmattie Persaud, operating through Fordham Fulton Realty. The portfolio is classic outer-borough rent-stabilized product — 262 apartments across four tax lots in Jamaica, Hollis, and Queens Village:

- 87-40 165th Street, Jamaica

- Six buildings along 215-01 to 215-15 Hillside Avenue, Queens Village (14 units)

- A cluster on 196-03 to 196-11 Jamaica Avenue and nearby 196th Street lots, Hollis (102 units)

- 88-02 197th Street, Hollis

The rents are modest, as you’d expect for the submarket:

- ~$1,311/month average on the Jamaica Avenue / 196th Street properties

- ~$1,736/month average on Hillside Avenue

The debt is not modest relative to that income: ~$36 million borrowed from Signature Bank in 2022. When Signature collapsed in 2023, the loans transferred to SIG RCRS A/B MF 2023 VENTURE, an entity associated with Santander Bank. Persaud was also named a political target by Mayor Zohran Mamdani.

⏳ The Timeline That Tells the Story

Follow the sequence, because the sequence is the lesson:

- Early 1990s — Two of the lots acquired. Long-held, presumably low-basis assets.

- 2022 — $36 million borrowed from Signature Bank against the portfolio.

- 2023 — Signature fails; loans transfer to a special-situations venture.

- November 2025 — Fordham Fulton Realty files for bankruptcy.

- June 2026 — Four foreclosure complaints filed in Queens County Supreme Court.

Layered on top: roughly $31 million in court-ordered penalties and fees for housing code violations. Read that against the $36 million in debt and the picture snaps into focus. The regulatory liability is nearly the size of the mortgage.

The lenders didn’t cite a single missed payment as the whole story. The complaints point to borrowers falling behind on debt service, insurance, water, and taxes — and to the housing code violations themselves as events of default.

That’s the part operators must internalize. The violations weren’t just an operating headache. They were a contractual trigger.

🧩 How a Portfolio Unravels

Distress at this level is almost never one thing. It’s a chain reaction:

- Deferred maintenance generates violations.

- Violations generate court penalties — here, ~$31 million of them.

- Penalties plus rising carry (insurance, water, taxes) drain the cash that’s supposed to service debt.

- Missed debt service hands the lender a default — and the violations give them a second default to cite.

- Bankruptcy buys time but doesn’t fix the underlying cash-flow hole.

- Foreclosure follows.

The economics underneath are brutally simple. On rent-stabilized product with ~$1,300–$1,700 rents, there is almost no margin to absorb a $31 million penalty overhang. The rent roll is capped by regulation. The expenses are not.

🎯 The Operator’s Takeaways

Whatever you think of the politics, the operational lessons are apolitical and precise:

- Compliance is capital preservation, not overhead. In a rent-stabilized portfolio, deferred maintenance doesn’t just annoy tenants — it manufactures penalties that can rival your loan balance. Treat your violation ledger like a debt schedule, because functionally it is one.

- Know your default triggers cold. Many owners assume “default” means “missed payment.” It rarely stops there. Insurance lapses, unpaid water and taxes, and code violations are frequently written in as events of default. Read the loan documents. Then re-read them.

- Underwrite the regulatory ceiling. When your rents are capped and your expenses aren’t, thin margins have no shock absorber. A single adverse cycle — a penalty judgment, a spike in insurance — can push a stabilized asset underwater fast.

- Lender transfers change the game. Persaud borrowed from a bank and ended up owing a special-situations venture. When a Signature-style failure moves your paper to a workout-minded holder, the counterparty’s tolerance for slow-pay evaporates. Know who actually holds your note.

- Political exposure is real risk. Being named a target concentrates scrutiny — from regulators, from the press, and from a lender deciding whether to work with you or foreclose. Reputation is a balance-sheet item.

💡 The Bigger Picture

New York’s rent-stabilized stock sits at the intersection of thin margins, heavy regulation, and expensive capital. This foreclosure isn’t a freak event — it’s what happens when all three pressures compound without a disciplined operating hand to manage them.

The owners who survive this environment aren’t the ones with the lowest basis or the friendliest politics. They’re the ones who treat compliance, carry, and covenants as a single integrated risk — and who never let deferred maintenance quietly metastasize into an event of default.

How are you stress-testing your stabilized portfolios against penalty and covenant risk right now? Share your framework below — this is exactly the kind of downside every operator should be modeling. 👇